A man wearing a face mask selects clothes at a market in Lusaka, capital of Zambia, on Aug. 18, 2020. Zambia’s confirmed COVID-19 cases have continued rising, with the total number close to the 10,000 mark.

Xinhua/Martin Mbangweta via Getty Images

Zambia has three weeks to improve transparency over its debt obligations and make progress toward an IMF-backed reform package, or risk defaulting on its loans.

Last week, a meeting of creditors was adjourned until Nov. 13 after a consortium comprising around 40% of Zambia’s Eurobond holders opted to abstain from voting on the country’s debt relief proposals, rather than voting them down.

Experts suggest bondholders are hoping the government can offer more clarity on its debt, particularly to China, and demonstrate progress toward an IMF program ahead of the Nov. 13 meeting.

“However, if no progress is made then there is no reason to suspect that bondholders will soften their stance, which will push Zambia into default when its grace period expires on 13 November and will signal a potentially acrimonious restructuring process ahead,” said Patrick Curran, senior economist at emerging markets consultancy Tellimer.

S&P Global Ratings on Thursday downgraded Zambia’s foreign currency rating to “selective default.”

“We view the nonpayment of debt service and the statement that the government will not make debt service payments as a default on its commercial debt obligations,” the ratings agency said in its update, forecasting that Zambia will remain in payment default for “at least the six months of the standstill period” as the government works toward debt restructuring.

How did Zambia get here?

On Oct. 13, the Zambian government announced it would suspend debt service payments to external commercial creditors, citing liquidity challenges compounded by the coronavirus pandemic. It has since failed to make an interest payment due on Oct. 14 for its 2024 Eurobond. Eurobonds are debt instruments denominated in any currency other than that of the issuer.

The government had on Sept. 22 asked Eurobond holders to agree to a temporary debt repayment freeze.

However, Zambia’s problems long predate the coronavirus crisis, with its economy constrained by structural factors such as low wealth, high fiscal deficits and a heavy debt burden.

LUSAKA, ZAMBIA – November 20: Edgar Chagwa Lungu, President of Zambia, on November 20, 2015 in Lusaka, Zambia.

Thomas Trutschel/Photothek via Getty Images

Tellimer’s Curran told CNBC that these issues had been compounded by “excessively lax fiscal policy” since President Edgar Lungu came to power in 2015.

“Over this period the budget deficit has averaged nearly 8% of GDP, driven mainly by a massive pipeline of Chinese-backed infrastructure projects,” he continued.

“With most debt denominated in dollars, sharp kwacha depreciation has exacerbated Zambia’s fiscal problems and pushed debt from around 36% of GDP in 2014 to 92% by the of 2019.”

While an IMF-backed reform package has been repeatedly promised by the government, it has consistently balked at austerity measures, and Curran said the country’s credibility has been “squandered” with the IMF and creditors.

Transparency and Chinese debt

Given Zambia’s pre-existing vulnerabilities, Curran suggested it should not be used as a bellwether for other African sovereigns post-Covid, but he said its restructuring effort could offer important lessons for other nations seeking bilateral debt relief.

In particular, the government’s seeking of private sector involvement is a first among countries included in the World Bank’s Debt Service Suspension Initiative (DSSI).

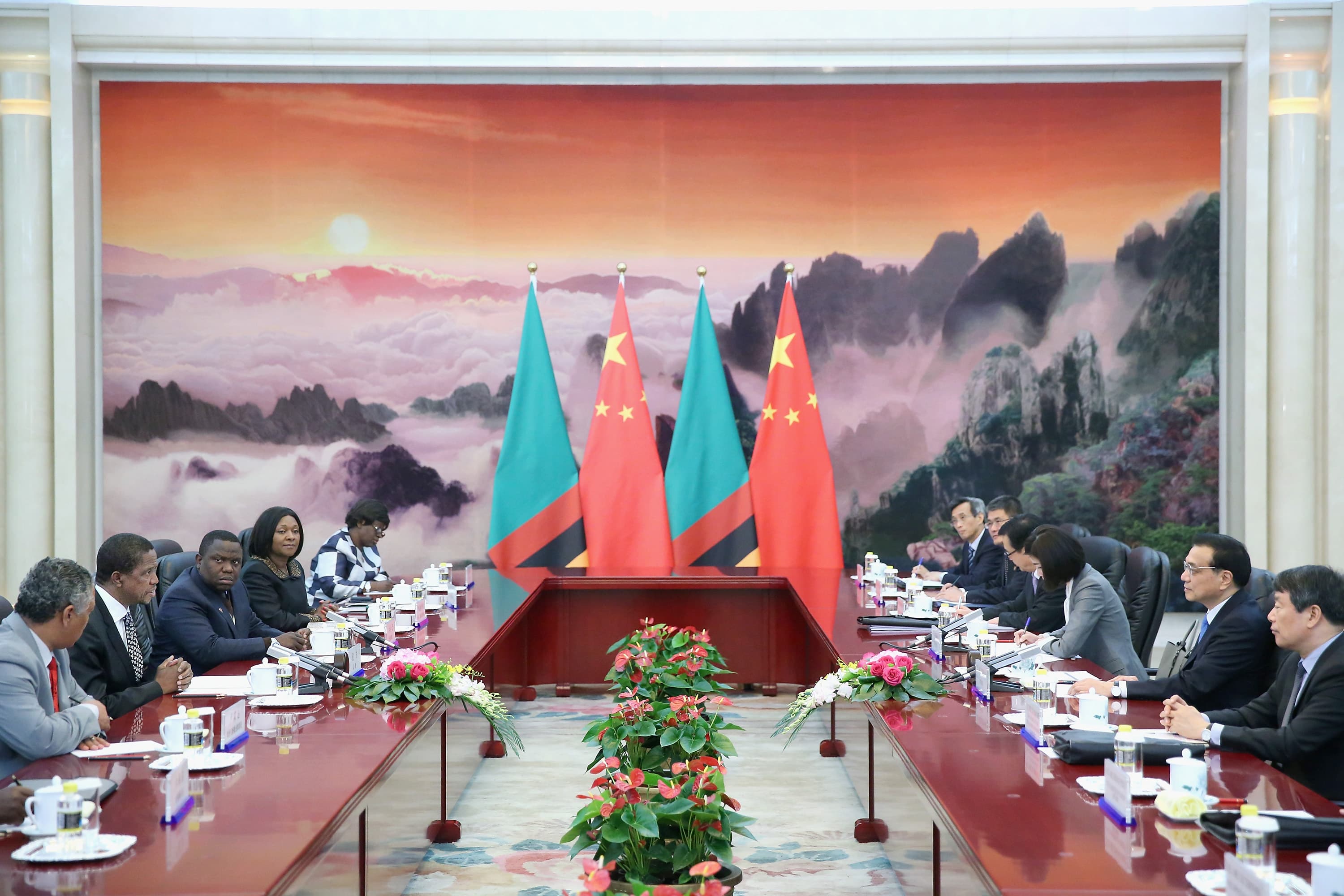

BEIJING, CHINA – MARCH 30: Chinese Premier Li Keqiang (2nd-R) meets Zambia’s President Edgar Chagwa Lungu (2nd-L) at the Great Hall of the People on March 30, 2015 in Beijing, China.

Feng Li-Pool/Getty Images

The key issue for bondholders remains a lack of clarity on the size, composition and terms of Chinese funding and assurances that an IMF program is imminent.

Although clearly problematic for Eurobond creditors, Zambia’s decision to skip payment seems to have found favor with Beijing, with Wu Peng, Director-General of the African Affairs Department at China’s foreign ministry expressing support via Twitter on Tuesday.

“The informational asymmetry between creditors – with Eurobond holders in the dark surrounding the extent of indebtedness to China, including the structure and negotiations progress with Beijing – remains a sticky point,” Irmgard Erasmus, senior financial economist at NKC African Economics, said in a note Wednesday.

Tellimer’s Curran told CNBC that a key concern for bondholders is that if they sign off on debt relief or restructuring without sufficient clarity on the existing stock of Chinese debt and terms of restructuring, then the cashflow savings will “simply be funnelled to Chinese creditors.”

“Zambia last issued a Eurobond in 2015, before debt began to spiral out of control, and most of the runup since then has been related to Chinese-funded infrastructure projects,” he said.

“From this perspective, bondholders could argue that they shouldn’t be responsible for doing the heavy lifting to put debt back on a sustainable trajectory.”

What happens if Zambia defaults?

In addition to the October payment obligation of $42.5 million, Zambia faces Eurobond debt servicing costs of $56.1 million in January 2021 and $20.2 million in March 2021, all of which it will be unable to pay.

“Under the strict assumptions that bondholders will insist on complete transparency on public and publicly-guaranteed (PPG) debt, in particular debt contracted by Zesco (Zambia’s state utility), we see a high risk of holdouts until restructuring agreements with large Chinese creditors (primarily EximBank) and/or a formal IMF programme have been reached,” NKC’s Erasmus said.

Zambia’s massive Chinese debt exposure is not unique, with Angola, Ethiopia, Kenya, Sudan and Nigeria all borrowing heavily to finance major infrastructure or research projects in recent years. Tellimer’s Curran pointed out that high Chinese debt reliance raises the chances of a “Chinese bailout, whereby bilateral relief is provided for strategic or geopolitical reasons and precludes the need for commercial restructuring.”

“This is what has happened in Angola, with Chinese debt relief freeing up space to service commercial obligations and helping to reduce scrutiny,” he said.

“However, if restructuring is required in other countries with significant Chinese debt, bondholders will need to be convinced that they are not being left in the dark on the amount and terms of outstanding Chinese debt and that it will not receive preferential treatment.”

NKC projects the Zambian economy will contract by 7.2% this year, a much sharper downturn than the -4.1% consensus, with a slow and drawn out recovery, assuming the country can avoid a protracted debt restructuring process which would drag the recession out through 2022.