“Economics is the science which studies human behavior as a relationship between ends and scarce means which have alternative uses,” the British economist Lionel Robbins wrote in 1932.

Put simply: Every choice comes with tradeoffs that might not be so savory.

It’s the position the Federal Reserve finds itself in as the U.S. central bank’s monetary-policy committee prepares to convene next week. The dilemma here is whether to fight inflation, risking the possibility that doing so triggers a recession, or to tolerate higher prices and keep the momentum going. Making a choice is easier said than done, with the ongoing Russia-Ukraine war raising the specter of stagflation – a combination of low growth and high inflation.

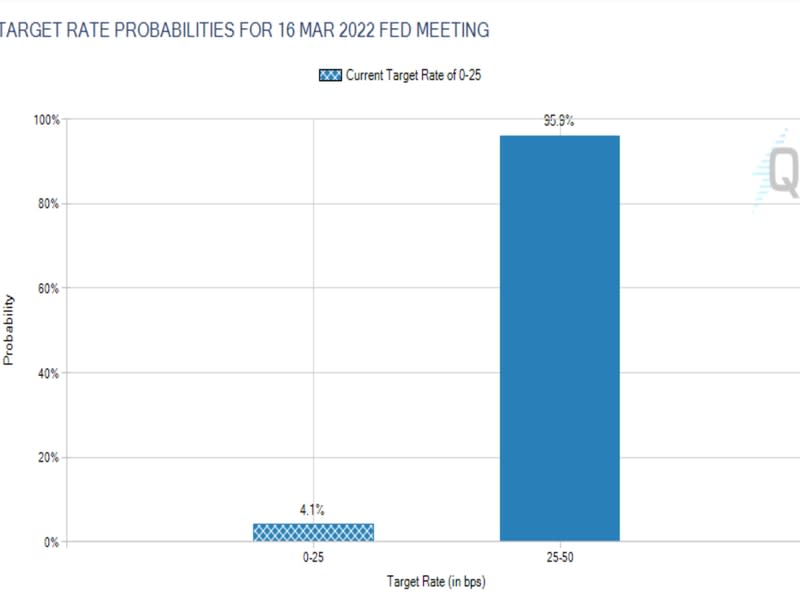

Observers say Fed Chair Jerome Powell and his colleagues will kick-start the tightening process with an interest-rate hike of 25 basis points (0.25 percentage point) next week while also signaling that they will push hard against inflation for the rest of the year. As always, they are expected to preserve their flexibility to adjust the pace if needed.

“Barring a very sudden tightening of financial conditions, as per February/March 2020, the Fed sticks to plan A, i.e., hike rates by 25 basis points next week,” Marc Ostwald, chief economist and global strategist at London-based ADM Investor Services International (ADMISI), said in an email.

“I think the Fed is very much going to echo the European Central Bank in trying to offer an element of predictability in what are very uncertain circumstances, while retaining optionality and flexibility,” Ostwald added.

Futures contracts on Fed funds imply a 25 basis point rate hike is already baked in to the market; it would be the first rate increase since December 2018. Two years ago, the central bank cut rates close to zero and launched an open-ended, liquidity-boosting, asset-purchasing program to counter the adverse economic effects of the coronavirus pandemic.

Fed’s dot plot to signal more rate hikes

Traders will look to Powell and the Fed statements for clues on how fast rates might rise in the coming months. The focus will be on the “dot plot” – a pictorial representation of Fed officials’ projections for the central bank’s key short-term interest rate. The officials also try to project the so-called terminal rate, which is the theoretically neutral interest rate that would both maximize employment and maintain stable prices.

In December, Fed officials contemplated 75 basis points of tightening for 2022 and a terminal rate of 2.5%. According to Marc Chandler, chief market strategist at Bannockburn Global Forex, these numbers could be revised higher next week.

“In the middle of December, 10 of the 18 officials expected that 75 basis point in hikes would be appropriate this year. Consider the terminal rate. In December, five officials expected that the Fed funds target at the end of 2024 would be above where the median viewed at the long-term equilibrium rate of 2.5%,” Chandler said. “The median is likely to rise by 50 basis points and maybe 75 basis points for this year.”

In other words, the Fed officials were behind the curve – or else the dynamic shows just how worrisome inflation has become in the past couple months. At press time, the Fed fund futures were anticipating a total of five quarter percentage point rate hikes for this year.

While some in the market fear that the Russia-Ukraine conflict will bring stagflation and force the Fed to hike aggressively, Michael Englund, principal director and chief economist at Action Economics LLC, suggests otherwise.

“Our assumption is that the updraft in commodity prices will diminish into mid-year, and base effects will finally allow an emerging downtrend in the year-over-year inflation metrics,” Englund told CoinDesk in an email. “This should diminish pressure on the Fed to address inflation, and should allow for quarter-point hikes at just every other meeting, leaving five hikes for 2022 overall (in March, May, June, September and December).”

Risk assets typically drop when a central bank is expected to hike rates. That’s because, while on the one hand, rate hikes bring down inflation, on the other, they weigh over individual and corporate spending, leading to an economic slowdown.

That said, the impending rate hikes may be old news, as the Fed has been preparing markets for the same since November. Bitcoin has declined over 40% since mid-November, predominantly on Fed rate hike fears.

“The interest rate market has already priced in as many as six rate hikes, and the crypto market is only pricing in more,” Griffin Ardern, a volatility trader from crypto-asset management company Blofin, said. “In my opinion, investors have not fully priced in the possibility of an early shrink of the balance sheet or quantitative tightening, say starting in April.”

Focus on quantitative tightening

Quantitative tightening (QT) is the process of balance sheet normalization, also a way of sucking out liquidity from the system.

The Fed’s balance sheet has ballooned from $4 trillion to $9 trillion in two years, thanks to the asset purchase program, known as quantitative easing, terminated on Thursday.

The process allowed the central bank to print money out of thin air and increase the supply of bank reserves in the financial system hoping that lenders would pass on the excess liquidity to the economy in the form of loans, bringing economic growth.

With inflation running hot, the central bank intends to reverse the process via quantitative tightening. It essentially means reducing the supply of reserves.

With the Fed likely to begin the hiking cycle next week, more details of quantitative tightening may emerge, as recently signaled by Powell.

“The process of removing policy accommodation in current circumstances will involve both increases in the target range of the federal funds rate and reduction in the size of the Federal Reserve’s balance sheet,” Powell said in his recent testimony to Congress.

“As the FOMC noted in January, the federal funds rate is our primary means of adjusting the stance of monetary policy. Reducing our balance sheet will commence after the process of raising interest rates has begun and will proceed in a predictable manner primarily through adjustments to reinvestments,” Powell added.

There are many opinions on how and when the Fed should start quantitative tightening and the pace of the unwind, with consensus ranging from $100 billion per month to $150 billion per month.

According to ADMISI’s Ostwald, the Fed may prefer gradual unwinding of the balance sheet. “My guess is they may opt for a tapering into QT to give themselves extra flexibility, though with larger increments, $25 billion then $50 billion, $75 billion and then $100 billion,” Ostwald said. “Their big challenge is that they want to have a strong element of predictability, but the current circumstances are very much antithetical to this.”

Bannockburn’s Chandler said, “the Fed will take the passive approach and allow the balance sheet to shrink, which means extinguishing some reserves by not reinvesting all of the maturing proceeds.”

Last week, Lorie Logan, executive vice president at the Federal Reserve Bank of New York, said the principal payments on Treasury bonds coming due range from about $40 billion to $150 billion a month over the next few years and average about $80 billion. There’s also an average of around $25 billion per month of mortgage-backed securities maturing for the next few years.

Risk assets may face selling pressure if the Fed hints at aggressive rate hikes or an early start to quantitative tightening. The Fed discussed QT in December and then pushed out the great balance sheet unwinding to the third quarter just before the war broke out in Europe.

“The hawkish risk is that the Fed’s statement wording is more aggressive than assumed, with little risk of either a larger rate hike and the start of quantitative tightening,” Action Economics’ Englund noted.

Will the Fed hold fire?

The obvious dovish outcome would be the Fed standing pat on interest rates and offering few clues on quantitative tightening. “Risk would rally if the Fed were not to raise rates,” Bannockburn’s Chandler said.

Many in the crypto community seem convinced that the Russia-Ukraine war and the recent asset market volatility would deter the Fed from raising rates. Some experts suggest otherwise.

“The Fed put is certainly out of action, above all because they are behind the curve on inflation, as they have implicitly admitted, and because of the asset price bubble that they have been feeding for so long (again indirectly admitted when talking about stretched valuations),” ADMISI’s Ostwald said.

The “Fed put” is the notion that the central bank will come to the rescue if assets tumble. The firm belief was evident in 2021 when retail investors consistently bought the dip in stock markets.

However, the Fed is unlikely to halt tightening unless signs of liquidity stress emerge in the global financial system.

“If financial conditions deteriorated sharply and suddenly in the context of other headwinds or risks materializing, yes, I think the Fed put, which means trying to offset the undesirable deterioration in financial conditions, broadly understood, is still there,” Bannockburn’s Chandler said.

“It says nothing about a 10% or 20% fall in a major equity index in absolute, but the recent drop, the Fed judged, in the current context not to adversely or unfairly tighten financial conditions,” Chandler added.

The above chart by Goldman Sachs shows that while financial conditions in the U.S. have tightened somewhat in recent weeks, the overall situation is still much better than the March 2020 crash.

It simply means the Fed is unlikely to hold fire next week.

“As long as there is no threat to the banking system, they [Fed] will not be unhappy seeing some of the leverage squeezed out of markets, but would certainly step back in (Fed put style), if feedback loops from the tertiary/shadow banking sector start to threaten the primary banking sector,” ADMISI’s Ostwald quipped.