Even professional investors are grappling with how to read markets in the pandemic.

The “striking” decline in the 10-year Treasury yield TMUBMUSD10Y,

Some investors worry the drop may be signaling a looming correction for equities that’s linked to concerns economic growth will slow as the pandemic drags on, said Naison-Tarajano, who also serves as global head of Goldman’s Apex family office business.

“Is the rate market telling us something that the equity market isn’t aware of yet?” she said. “We’re going to watch it very quickly,” said Naison-Tarajano, though at this point, she’s not sure the recent slide in the 10-Year Treasury yield should be of “extreme concern” for clients.

“We are advising clients to certainly keep their holdings in equities,” said Naison-Tarajano. “If you had panicked and sold” equities over the past year plus, she said, “it’s impossible to make up the returns that we’ve experienced.”

Major U.S. stock indexes are trading near record highs and haven’t seen a big pullback in months. The S&P 500 SPX,

But “stocks aren’t performing as well as you might expect on the back of some really good earnings” reported for the second-quarter, said Naison-Tarajano, suggesting concerns over the spread of the more contagious delta variant of the coronavirus may be dampening sentiment.

While “relatively optimistic on equity markets” in advising clients to stay invested, Naison-Tarajano said she is not recommending adding a lot more exposure.

“One thing I would be wary of right now is leverage with equity markets,” she said. With the stock market up significantly this year, and uncertainty surrounding rates, she said “we just don’t want anyone to be in a position where they’re going to be a forced seller on a correction.”

Buying dips in U.S. stocks, on the other hand, is the type of opportunity “we definitely would look for,” according to Naison-Tarajano. She said that she recommends buying dips in mega-cap growth stocks that are benefiting from secular digital trends, as well as “oversold reflation trades.”

Read: Is the reflation trade over? What stock-market investors need to watch

Goldman’s private-wealth clients tend to have a long-term view of their holdings, according to Naison-Tarajano, who said she guides them with a thematic approach to investing.

“Our clients tend to be pretty overweight equities and with rates this low I’m not sure there’s really anywhere else to go,” she said. Given the market has been “quite confusing” following a “volatile” 2020, she added, “we do see relatively high cash balances.”

That’s generally good for when markets dislocate, as it sets up clients to be opportunistic, according to Naison-Tarajano, who said she considers U.S. Treasurys to be cash equivalents. That’s because Treasurys have a stable net asset value and clients can trade out of them on a daily basis, she explained.

Puzzling drop in yields

The yield on the 10-year Treasury note was trading around 1.2% Thursday afternoon, tumbling from about 1.7% as recently as May 12, FactSet data show. Federal Reserve Vice Chair Richard Clarida said Wednesday he was surprised by the size of the decline in bond yields since the spring, MarketWatch reported.

Yields are low despite strong economic growth and surges in inflation. Fed Chair Jerome Powell has repeatedly described the rise in the cost of living as transient, saying it’s linked to the rebound from the pandemic.

Goldman expects the 10-year Treasury yield to rise to 1.9% this year, said Naison-Tarajano.

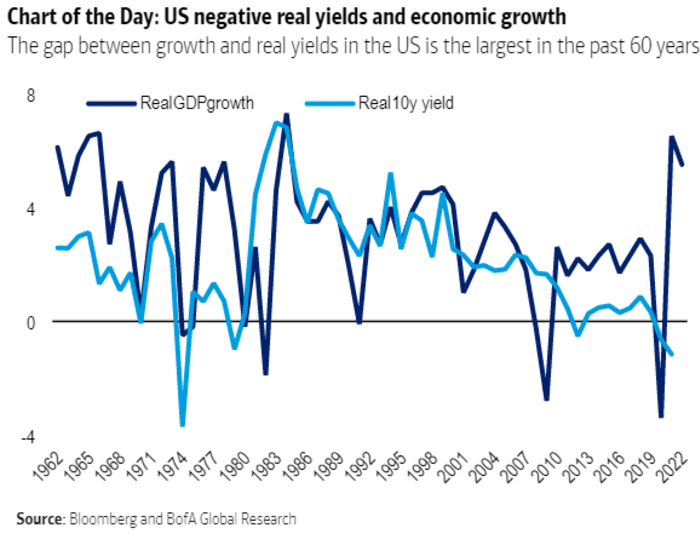

But the pandemic has pushed “real yields” — or nominal yields minus core inflation —- to a negative level in the U.S., according to a BofA Global Research report this week. “The puzzle is that they continued falling during the recovery this year, which is historically a first,” BofA strategists led by Athanasios Vamvakidis said in the note.

BofA Global Research

“U.S. real yields are the most negative since 1974, despite a strong U.S. recovery,” the strategists wrote. “Nominal rates are also low, but higher than last year, suggesting higher inflation is part of the explanation in the U.S.”

Read: Here’s how often ‘inflation’ is being mentioned on corporate earnings calls

According to the BofA report, real yields and growth should be close “in theory.” The analysts noted that “U.S. GDP has already reached its pre-COVID-19 level.”

In the past 60 years, real yields on the 10-year Treasury yields “have been negative only during severe global shocks, including the two oil price shocks in the 1970s and the Eurozone crisis in 2012,” according to the BofA research report. “In the past, U.S. real yields never stayed negative for more than a year,” the strategists said.

Check out: Stagflation is ‘a legitimate risk’ that would be painful for U.S. markets

For private clients worried about rising inflation, hard assets such as real estate may be one area to consider adding exposure for protection, according to Goldman’s Naison-Tarajano.

In the meantime, positive nominal yields for U.S. Treasurys, however low, may still look attractive next to negative yields on other sovereign bonds such as in Europe, according to Naison-Tarajano. The yield on 10-year German government bond, for example, is trading at a negative rate.

“If you want to have cash to stay nimble to act when the market dislocates and be opportunistic, said Naison-Tarajano, “I’m still very supportive of holding” some Treasurys. Maybe not as much as 40% of portfolios, she said, but some exposure is “ok” even if it means earning “very little.”