David Rosenberg: Slumping equity risk premiums mean there is more bear market to come

An unusual selloff period compared with history

Article content

By David Rosenberg and Marius Jongstra

Advertisement 2

Story continues below

Article content

For the better part of the last cycle, going back to 2009, investors have turned to the equity risk premium (ERP) in the United States as a key rebuttal against claims of overvaluation, arguing low levels of bond yields make the stock market more attractive in comparison. This validation, that “there is no alternative” (TINA), has completely evaporated with the rise in interest rates.

Article content

Article content

At current levels, investors can garner a four-per-cent yield on the two-year T-note, or more than 3.5 per cent on the 10-year. In comparison to bonds, the stock market is back to its least attractive since late 2007, with the additional compensation for risk at just 270 basis points.

Despite the S&P 500 being in the middle of a 20 per cent or so correction, the ERP has contracted since the market peaked back on Jan. 3. Using history as a guide, this is highly unusual, since it typically needs to widen by +425 basis points, on average, before bear markets come to an end. Until such a development occurs, it is best for investors to fade the calls of a market bottom as, by this account, the risk/reward profile remains unfavorable with more downside ahead.

Advertisement 3

Story continues below

Article content

Interestingly enough, after initially expanding following the market peak on Jan. 3, the risk premium began to significantly contract as the surge in bond yields dwarfed the improvement in the S&P 500 earnings yield. Note that our definition of the ERP is calculated by subtracting the 10-year Treasury yield from the S&P 500’s forward earnings yield (also known as the Fed Model).

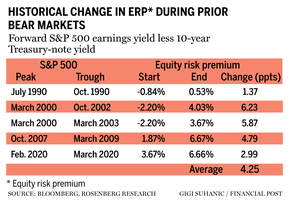

Plotting the path of this current episode compared to the average and the range of prior bear markets, using Bloomberg data back to 1990, it becomes clear how unusual this selloff period has been compared to history, as well as how much work needs to be done to get caught up. At a little more than 180 trading days since the highs, the ERP has compressed by 30 basis points compared to the historical average of a 100-basis point widening that has typically taken place.

Advertisement 4

Story continues below

Article content

Our work shows that a trough is not put in until the ERP widens by 425 basis points. More importantly, while the range varies from +137 basis points to as much as +623 basis points, no bear market has bottomed without an ERP that has expanded at all. Even at the mid-June lows, the increase in the equity risk premium was a lowly 30 basis points, to just over 300 basis points. That’s a far cry from the historical average change and, on a level basis, represented a 70th percentile reading in the post-quantitative-easing period. Such a modest improvement, to a still historically elevated level, does not point to a market bottom in our view.

It cannot be denied that this corrective phase has followed a different pattern than similar periods in the past, no thanks to the current inflationary pressures and the upward influence on bond yields. And while there are many moving parts to how the ERP can normalize, it is unlikely the stock market will be untouched, especially with the lagged effects of the U.S. Federal Reserve’s tightening having not been fully reflected in the corporate profits outlook.

Advertisement 5

Story continues below

Article content

For illustrative purposes, if we assume an equal split in terms of contribution from stocks and Treasuries towards an expanding ERP, achieving a +425-basis point change translates to a fall in the 10-year U.S. Treasury yield towards 1.5 per cent alongside an approximately 20 per cent drop in the S&P 500 from current levels. Should interest rates prove more resilient, stocks would have to fall even more.

As always, while our analysis focuses on the headline level, it doesn’t mean there aren’t opportunities beneath the surface for investors to explore. In the accompanying table, we calculated the ERP across the various S&P 500 sectors as defined by the forward earnings yield less comparable investment-grade bond yields (a.k.a. using a modified Fed Model approach). Two key findings appear.

Advertisement 6

Story continues below

Article content

First, on an absolute basis, only five sectors offer any kind of meaningful yield pick-up relative to their comparable bonds: energy (a premium of 7.9 percentage points), financials (2.7), materials (2.6), health care (1.4) and communication services (one). The remaining group (industrials, consumer staples, utilities, technology and consumer discretionary) have earnings yields in-line with, or lower than, their corporate bond equivalents, meaning investors are better off buying the fixed-income products of these companies since there is little-to-no extra compensation for equity risk.

-

David Rosenberg: A Canadian recession is ‘all but set in stone’

-

Noah Solomon: Investors should think again if they believe alternatives are a portfolio panacea

-

Better governance, oversight give reasons to remain optimistic about the future of ESG investing

Advertisement 7

Story continues below

Article content

Second, from a forward-looking basis, what jumps out is just how historically compressed the ERP is in many sectors. Every sector except for energy and materials is at an extreme percentile reading, meaning the likelihood of continued compression is significantly smaller.

Ultimately, the ERP is just another valuation tool, which does not offer great timing abilities, but does provide a window into what future returns look like. On this basis, in terms of equity exposure, energy and materials appear the most attractive.

However, it is clear the stock market overall has yet to sufficiently reprice to account for rising interest rates. Against this backdrop, the path of least resistance for the S&P 500 is likely to remain to the downside. What has happened with the ERP to date is simply insufficient to call a bottom just yet.

David Rosenberg is founder of independent research firm Rosenberg Research & Associates Inc. Marius Jongstra is a senior economist and strategist there. You can sign up for a free, one-month trial on Rosenberg’s website.

_____________________________________________________________

If you like this story, sign up for the FP Investor Newsletter.

_____________________________________________________________

Advertisement

Story continues below