However, Griffin says, the notion that the industry has already entered a supercycle and talk of structural deficits may be premature at the moment.

The supercycle is yet to launch, says Griffin, and after a period of restocking (and hoarding in some instances) this year and next, tightness in most markets will ease including lithium and battery raw materials. Notable exceptions are zinc and aluminum, which will be affected by power issues in China and Europe.

Further out to the end of the decade, the demand picture remains healthy underpinned by post-pandemic economic recovery and supply worries amid the energy crunch in Europe and China:

“When you look out to 2030, structural demand issues associated with the energy transition really start to have an effect.”

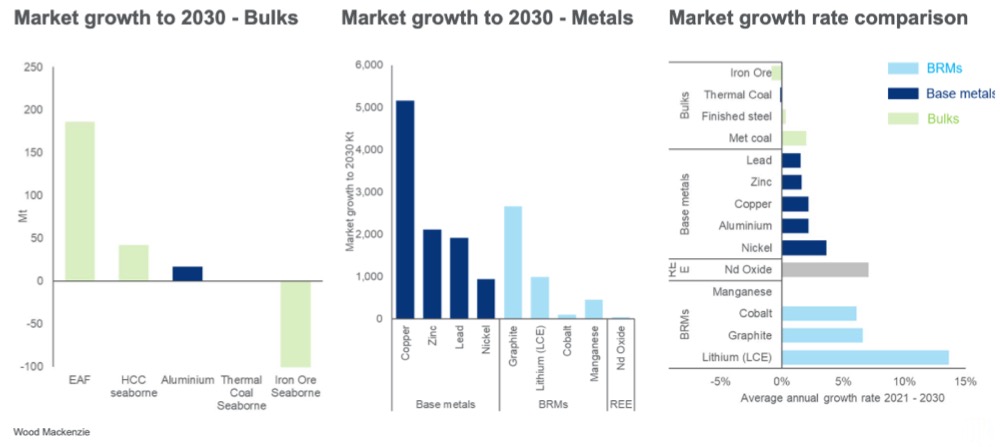

Woodmac sees growth for lead and zinc in the 50% range, roughly 20% for copper and aluminum, 40% for nickel and 70–80% for rare earths, cobalt and graphite out to 2030. The lithium market is expected to triple in size over the same period.

The 2030 outlook is less kind to iron ore where the seaborne market could see as much as a 100 million tonnes decline in annual shipments. Thermal coal markets will stagnate and the steel market will only show slight growth.

In absolute terms, Woodmac projects an additional 5 million tonnes of aluminum and copper demand, while the lithium market is expected to grow by 400,000 tonnes and cobalt by some 40,000 tonnes.

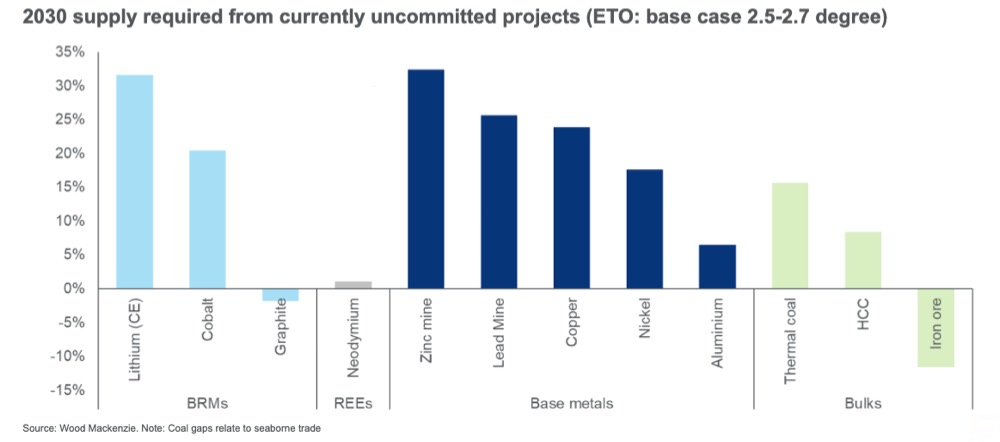

The significant jump in required metals necessitates a supply response which Woodmac estimates will require additional investment of about $200 billion. Griffin says reluctance from an investment perspective is understandable given the high volatility in the market, particularly for those commodities heavily influenced by China:

“We can understand that miners may not wish to dive in with both feet but something has to change because we are in 2022 and 2030 is just around the corner – particularly when it takes typically 7-10 years to bring on new greenfield supply and over 10 years from first discovery to first metal.”

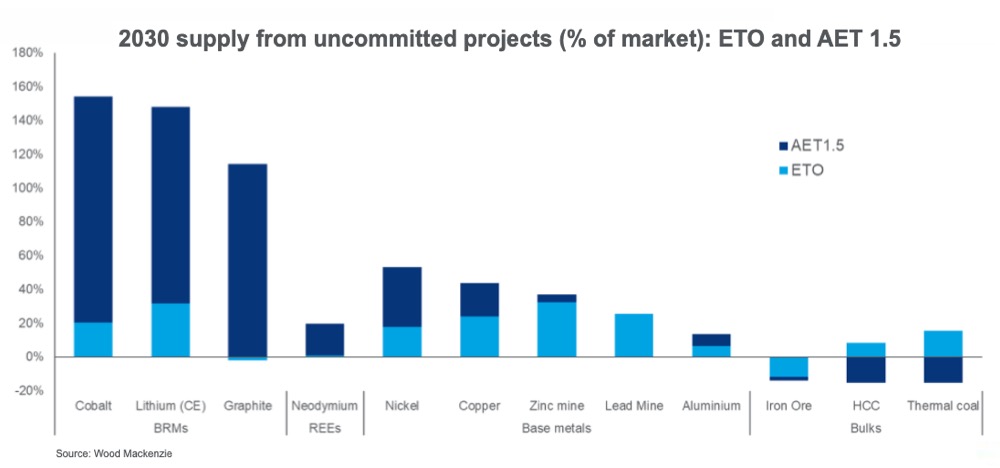

Griffin says this growth is expected under Woodmac’s base case green energy transition scenario where global temperatures rises are limited to 2.5–2.7 degrees celsius through 2050. Under the goals of the Paris agreement the needed metal jumps significantly, putting extraordinary pressure on metals supply and needed capital expenditure balloons to some $400 billion.