Demand is being driven by the much greater range (and sometimes driving range) of models on offer – not that long ago, to misquote Henry Ford, you could have any electric car you wanted, as long as it was a Tesla.

Kilo what?

Range remains the number one concern for prospective buyers – even the CEO of Volkswagen felt it necessary to complain about the lack of charging infrastructure on a trip in Italy. Steadily decreasing battery prices and changing chemistries made it possible to address range anxiety with bigger packs and greater energy density.

From nearly $300 per kWh in 2014, prices for lithium ion batteries (with nickel-cobalt-manganese (NCM) chemistries) came close to the pivotal $100 mark, where electric cars reach cost parity with gasoline powered vehicles.

But with battery raw material prices soaring – particularly lithium – this year is likely to see the trend reversed with battery costs increasing on kWh basis.

The battery can be as much as 40% of the overall cost of an EV, and as such, raw material prices have a much greater impact on EV costs relative to internal combustion engine (ICE) vehicles.

Material world

Combining data from Benchmark Mineral Intelligence, a London-Headquartered price reporting agency and battery supply chain consulting firm and Toronto-based Adamas Intelligence, which tracks demand for EV batteries by chemistry, cell supplier and capacity in over 100 countries, MINING.COM examined how the increase in metal prices may affect costs for automakers.

Only full battery-electric vehicles are considered, hybrids and plug-in hybrids are excluded, which explains the complete absence of Toyota from the rankings. To produce the most accurate data, the battery metals deployed numbers in the tables do not include cars leaving assembly lines, those on dealership lots or in the wholesale supply chain, only end-user registered vehicles.

That means that the tonnes of lithium, graphite, cobalt, manganese and nickel used in the calculations would have entered the battery supply chain at the latest six months ago at a time when prices were still relatively subdued. The tonnages reflected in the end-product are fractions of what would have been procured upstream.

Factories floored

Battery manufacture is a notoriously tricky business. A factor that is sometimes omitted from estimates of metal demand is low yields in the manufacturing process.

Tesla’s main provider Panasonic outlined an average 39% quarterly cell production loss against apparent capacity in the early years of the Nevada gigafactory, for instance. And anode and cathode makers certainly drop stuff on the factory floor, too.

And you don’t want to get it wrong – on a per vehicle basis Hyundai’s recall of its Kona for a battery replacement cost $11,000 per vehicle.

LG Chem says they’re not to blame for the Kona problems, but the Korean battery maker is footing the bill for GM’s $1.9 billion recall of most of its Bolts. The pricey recalls are another indication of just how much the battery represents of the total value of your average EV.

The tonnages (all 100% contained metal basis except lithium, which is lithium carbonate equivalent) reflected in the final product also comes after conversion processes, which are also accompanied with losses in yield. Chinese chemical processors and refineries are known for converting to and fro as market demand changes (and in the dynamo Chinese market that is often).

All of which is a roundabout way of saying not not all that much coming out of Wodgina, Tenke Fungurume, Sorowaku, Balama and N’chwaning makes it all the way into the Skywell Chuangyezhe showroom in Zibo.

LFP LMFAO

Apart from the effect of rising prices, another striking feature of the year in EVs is the changing mix of chemistries, and particularly the runaway success of cheap and cheerful lithium-iron-phosphate (LFP) first outlined by MINING.COM in March last year.

While NCM (nickel-cobalt-manganese) and NCA (nickel-cobalt-aluminum) still account for most of the market and LFP compares badly against ternary cathode batteries in terms of energy density and therefore driving range, uptake of LFP has been rapid.

From a standing start little over a year ago, in 2021 nearly one out of every five electric cars sold sported an LFP battery, which apart from being cheaper also lasts longer. And that is without a single LFP model available in North America.

China’s BYD confirmed in April that it’s going all-in on LFP scrapping NCM technology from its model line-up entirely. BYD, which is backed by Warren Buffet through a 21% stake, is the second-largest electric vehicle brand by volume and also supplies other carmakers with its battery technology.

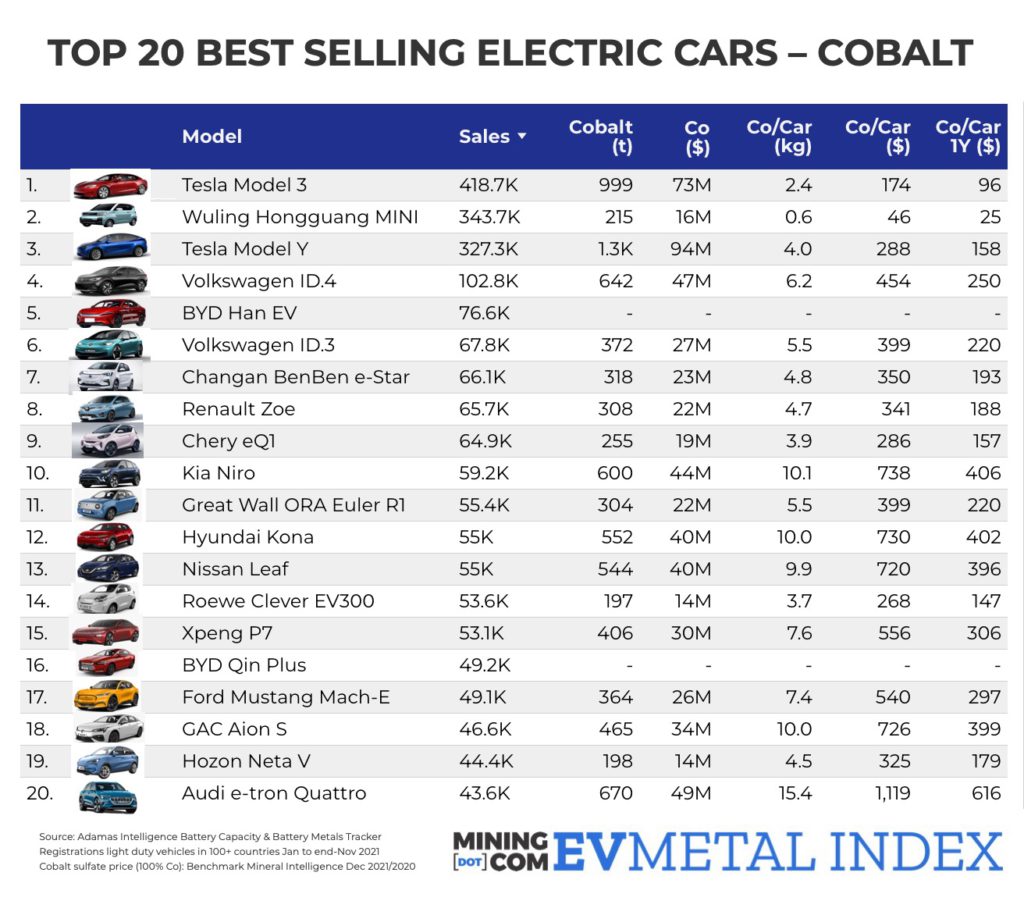

As the charts show, the BYD Han in comparison to the Tesla Model Y is able to avoid more than $1,200 nickel, cobalt and manganese costs per vehicle and that is despite the fact that LFP already makes up 14% of global Model Y sales after just four months on the market in China.

Hong today guang tomorrow

Perhaps the most striking example of how battery size and composition affects the end-product in the electric car industry is the number two ranked vehicle of 2021 – the Hongguang MINI.

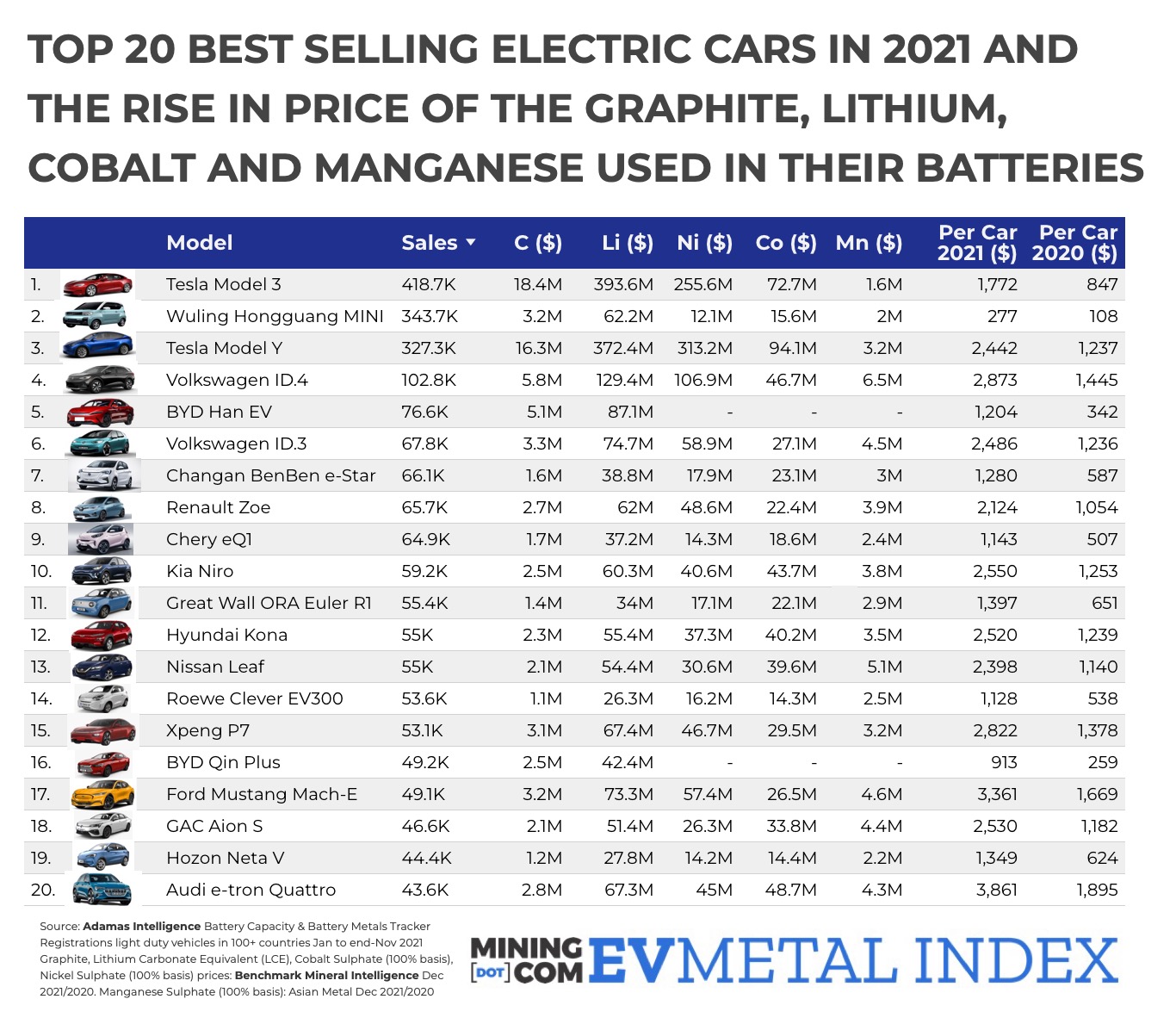

The boxy runabout is a joint venture between China’s state owned SAIC, General Motors and Wuling with a base price of less than $5,000. The cost of the battery metals used in the Hongguang MINI totals $277 per vehicle based on today’s prices for lithium, graphite, nickel, cobalt and manganese.

That compares to $1,772 for the Model 3. A total of six different manufacturers supply the battery for the tiny car with battery capacity. The low cost is not only due to the fact that 60% of the Hongguang MINIs sold last year were equipped with LFP batteries vs one out of three Model 3s sold globally.

Mainly it boils down to battery size. Some Hongguang MINI’s are equipped with batteries packed with only 9.3kWh versus 62.3kWh for the Model 3. Compare also the Model 3’s battery metals costs against brawnier NCM-equipped competitors – the Audi e-tron Quattro at nearly $3,900 and the Ford Mustang Mach-E at nearly $3,400, both of which also use more cobalt-rich cathode chemistries.

For a high-end vehicle or sports car, a $1,500 or $2,000 jump in raw material costs may not affect automaker margins or sticker prices that much, but at the lower end these are substantial cost increases especially keeping in mind that the tonnes in the road-going car battery are not nearly what had to be procured upstream.

Counting carbonates

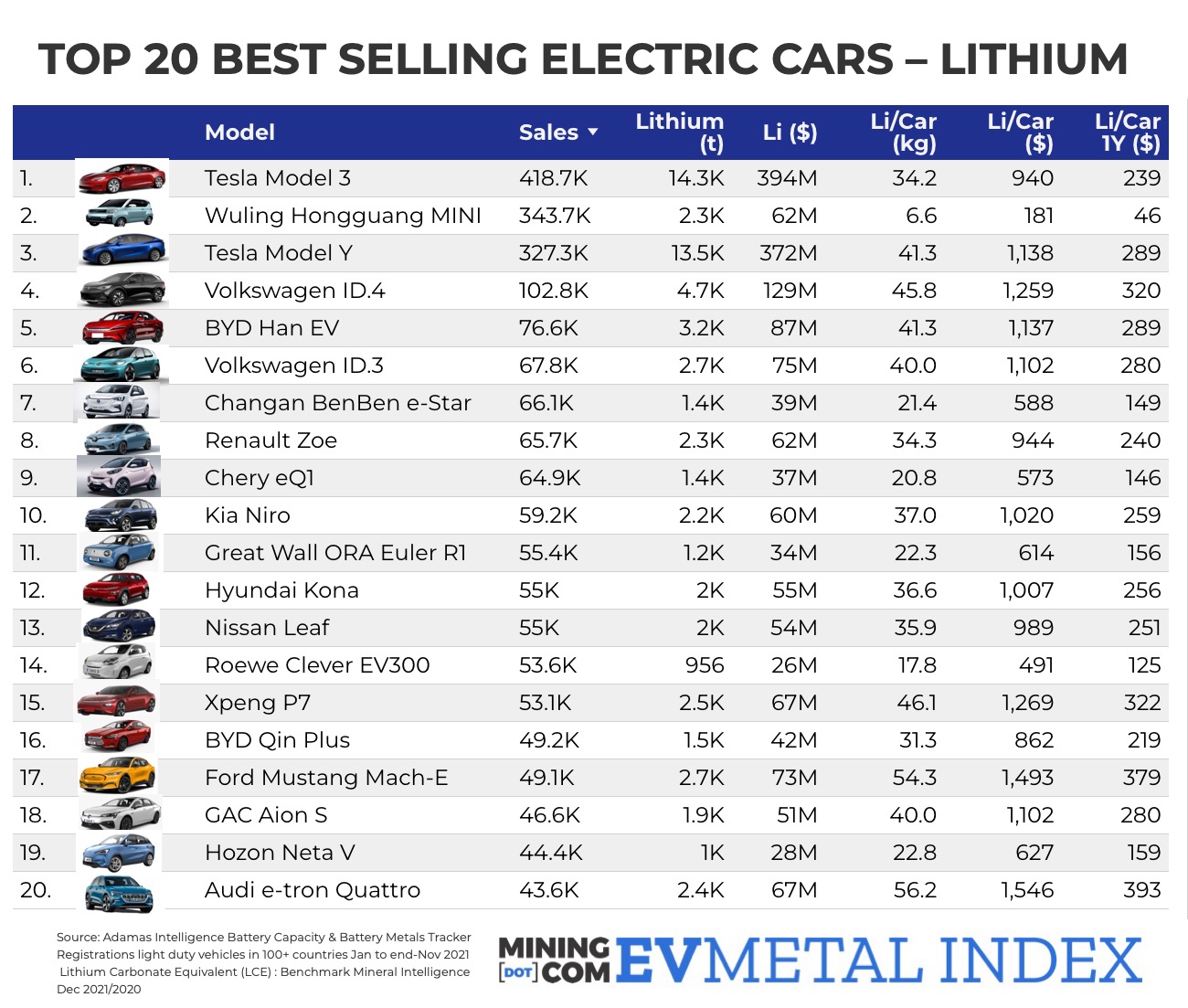

That said, LFP’s relative cost advantage is somewhat flattered by the global weighted average lithium price used in these calculations.

Lithium prices have jumped across the board over the past year, but a massive gap has now opened up between ex-works prices in China for minimum 99.5% battery grade carbonate, which have quadrupled to nearly $40,000 a tonne, according to Benchmark December averages.

That compares to European prices for carbonate of $18,500 (CIF minimum 99%). Benchmark also points out that the premium of lithium carbonate over lithium hydroxide – used in high nickel cathodes – reached $6,600/tonne in December. Historically, hydroxide has always been the pricier one.

Installed LFP battery manufacturing capacity in China, where nine out of ten LFP batteries are manufactured, tripled last year. Using ex-works prices in China instead of the global average for lithium closes the cost gap substantially to NCM batteries.

Nickel adds dimes

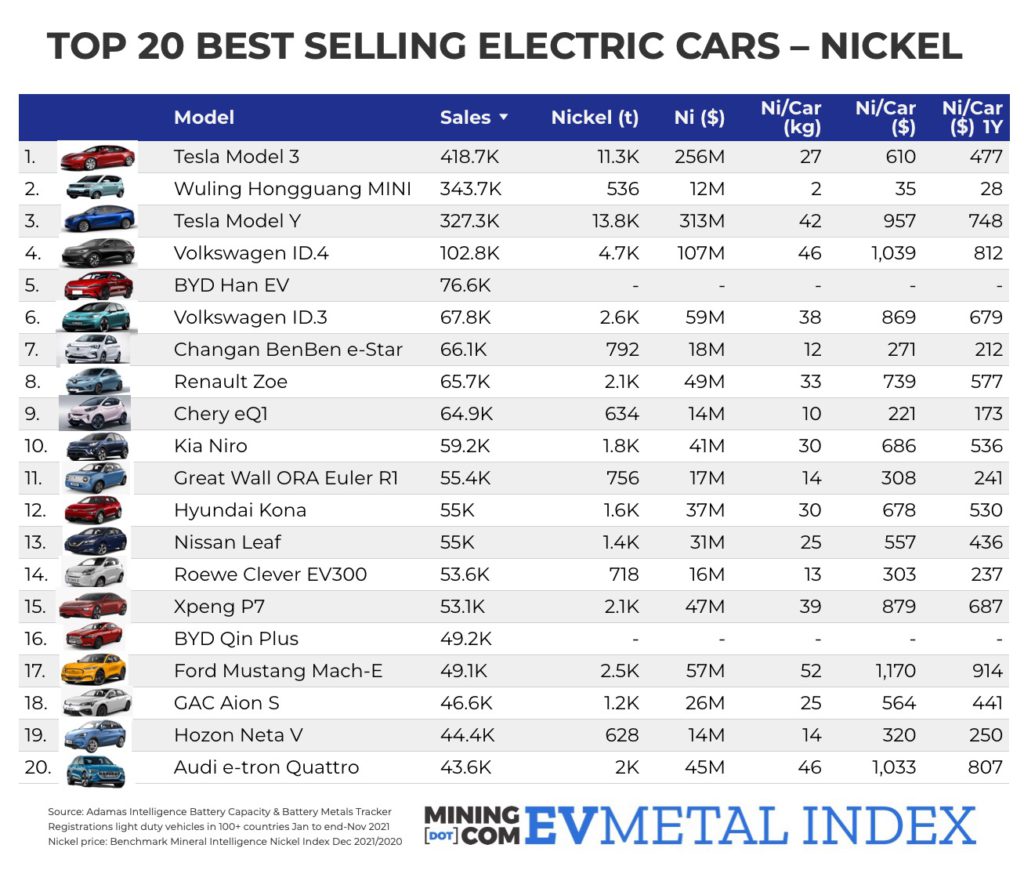

Nickel has had a typically volatile year and prices are more likely to follow developments in the stainless steel industry than EVs.

Prices are back at 10-year highs above $22,000 despite Tsingshan making good on its promise to meet the demands of the EV market by converting nickel pig iron into matte suitable for the battery supply chain.

Benchmark believes battery grade nickel from this source would not play a major role outside China due to environmental concerns about the carbon-intensive conversion process and the US adding nickel to its critical mineral lists is further evidence of continued strong demand from the auto sector.

Cobalt prices bolt

Cobalt prices are up more than 70% over the past year to the highest since August 2018, when the metal was coming off all-time highs above $100,000 per tonne.

That is despite the best efforts of automakers to thrift cobalt loadings by opting for LFP in lower end models and moving to NCM 811 chemistries (NCM 111 with equal parts nickel, cobalt and manganese now accounts for only 3% of the market)

Still, Benchmark believes NCM will remain the dominant technology outside China, volume growth in electric vehicles will offset other forces and demand for cobalt should grow at a 13% compound rate over the next ten years.