Stock market investors still aren’t sweating rising inflation pressures that saw U.S. consumer prices rise 6.2% year-over-year in October, a nearly 31-year high. And that might not change until the Federal Reserve gets more aggressive, analysts said.

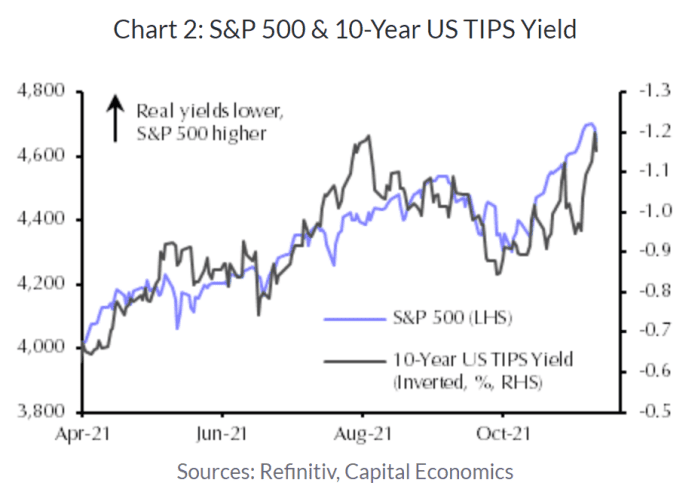

“U.S. equities have shrugged off this year’s surge in inflation, probably because it has not coincided with either a rise in the real yields of Treasurys or weakness in corporate earnings,” said Oliver Allen, markets economist at Capital Economics, in a Thursday note. The real yield is the yield an investor receives after accounting for inflation.

Mark Hulbert: Inflation is boosting prices and stocks — here’s why that isn’t a surprise

Markets were briefly roiled following the October Consumer Price Index reading on Wednesday. Nominal Treasury yields rose sharply, weighing on stocks, particularly technology and other growth-oriented sectors seen as most sensitive to rising interest rates.

Equities put in a stable performance Thursday, while the Treasury market was closed for the U.S. Veterans Day holiday. The tech-heavy Nasdaq Composite COMP,

All three major indexes remain not far off all-time highs, coming off a robust third-quarter earnings season that saw companies maintain profit margins and maintain relatively upbeat guidance.

Inflation, of course, isn’t necessarily a negative for equities. Stocks are viewed as real assets, which means they tend to appreciate in an inflationary environment, making them a useful hedge against inflation pressures.

Related: Hot inflation undercuts one of the main arguments against stocks. Here’s why.

However, inflation well above the low single digits, as was the case in much of the 1970s and early 1980, has tended to coincide with lower stock-market valuations due to the negative effects of rising prices on economic growth or the Fed tightening monetary policy to bring inflation back down, Allen noted.

But despite inflation running in what would appear to be the danger zone, Allen noted that real, or inflation-adjusted interest rates, haven’t risen significantly at either the short or long end of the yield curve.

While the October CPI release prompted a small rise in the yield on 10-year U.S. Treasury inflation protected securities on Wednesday, the general pattern of the past six months has been characterized by falling real yields that have appeared to push U.S. equities higher, Allen said (see chart below).

Meanwhile, the sharp, one-day rise in the 10-year Treasury yield and moves in fed funds futures on Wednesday reflected expectations the Fed will accelerate the wind-down of its asset-buying program and begin lifting its policy interest rates in 2022 sooner and more aggressively than expected. But it didn’t indicate investors fear a long-lasting run of high inflation, said Nicholas Colas, co-founder of DataTrek Research, in a Thursday note.

The market action on Wednesday “was all about investors adjusting their views on Fed policy. If [investors] really thought plus-6% inflation was the ‘new normal,’ asset prices would be much, much lower,” Colas wrote.

And while the breakeven rate on five-year Treasury inflation protected securities hit a new high, they’re still signaling expectations for inflation of just 3% over the next half-decade, he said.

Archive:‘Good’ inflation or ‘bad’? Investors are scared because they can’t tell the difference

Some investors do fear the Fed has already lost control of inflation and inflation expectations. As result, policy makers may need to tighten monetary policy much more aggressively than anticipated, potentially leading to a sharp economic downturn.

But some stock-market watchers expect stocks to remain supported until policy makers show signs they’re prepared to take more aggressive action.

The rise in bond yields on Wednesday marked a bounce from a sharp two-week decline that wasn’t based on fundamentals and was, therefore, unlikely to last, said Tom Essaye, founder of Sevens Report Research, in a Thursday note.

“During that period, tech rallied and led markets higher, and we’re seeing both trades now unwind. And given tech’s large weighting, that will be a headwind on the S&P 500,” he said.

“But unless the Fed starts strongly hinting at an accelerated taper or a much- sooner-than-expected rate hike, we do not see yesterday’s hot CPI or rise in yields as a reason to get more defensive,” he said, arguing it was instead reminder of the dominant trends in the market: above-normal inflation and rising yields.

A policy shift by the Fed could come before year-end, potentially spelling trouble for stocks, warned Jeremy Siegel, finance professor at the University of Pennsylvania’s Wharton School. in a CNBC interview on Wednesday.

“Listen, stocks love inflation until the Fed gets serious about it and they have not been serious about it,” he said, warning that more inflation data in line with the October report before the central bank’s mid-December policy meeting would put “enormous” pressure on Chairman Jerome Powell “to come down much stronger than he has so far.”

Allen said Capital Economics expects the Fed to follow through with a “modest tightening in the real stance of monetary policy,” accompanied by a grind higher for U.S. TIPS yields.

“The tailwind of falling real yields turning into a modest headwind is one reason why we think U.S. equities will struggle to make gains over the next couple of years,” Allen wrote. “Another reason is that we think the recovery in the US economy will fall short of investors’ expectations.”