COVID-19 cases may cause an S&P 500 correction, analyst says. Buy these stocks in the next dip.

It’s a rough start to the week for markets. Stocks sold off in Asia and Europe, and Dow industrials futures tumbled more than 300 points setting the tone for a turbulent day ahead.

Blame rising COVID-19 cases globally, and the spread of the more infectious delta variant of coronavirus.

What we’re seeing in markets is a “July chop” triggered by the delta variant, according to analyst Thomas Lee of Fundstrat Global Advisors. Our call of the day is from Lee, who said that delta variant concerns could lead to a 5% correction for the S&P 500 SPX,

Daily U.S. COVID-19 cases are approaching the 30,000 mark, but there is a risk that infections could go “parabolic” with the spread of the delta variant, and rise to around 100,000, Lee said.

The delta variant could create panic, because markets and investors typically focus on case counts as opposed to hospitalizations, Lee said — and as many as 82 million Americans remain unvaccinated or without COVID-19 antibodies. However, hospitalizations remain low.

This delta variant has a lot of “bark” and is unnerving for investors, Lee said, even if there’s not a strong “bite.” It could add weight to a “July chop” that has history on its side. Since 1928, a strong first half of the year leads to a flat or negative July.

While the S&P 500 was up 0.7% in July as of the end of last week, “this belies the violent sector rotations taking place within the broader market,” Lee said.

The Fundstrat analyst said that he doesn’t expect the chop caused by the delta variant to cause a 10% or larger decline in stocks, but a 5% drop for the S&P 500 is possible.

So while there’s little reason to be hugely bearish — because bond spreads indicate wider stability for stocks, and volatility measures are not signalling broader weakness — this “vicious” risk-off correction creates opportunities.

Lee is bullish on “epicenter” stocks — shares in companies battered by the pandemic and set to benefit from the reopening — like travel, consumer discretionary, energy, and basic materials. As well, Fundstrat is overweight on Big Tech, with the likes of Facebook FB,

The buzz

Billionaire investor Bill Ackman’s blank-check, special-purpose acquisition company Pershing Square Tontine Holdings PSTH,

On the U.S. economic front, investors can expect the National Association of Home Builders’ housing market index for July, which measures the market conditions for the sale of new single-family homes.

OPEC+, the group of oil-producing countries including Russia and Saudi Arabia, agreed on Sunday to further relax oil production cuts as demand for crude continues to rise and price soar. Production will rise by 400,000 barrels a day each month beginning in August and will eventually undo all of the pandemic-era curbs.

Zoom plans to buy Five9 FIVN,

The markets

U.S. stocks look set for a rough day ahead: Dow industrials futures YM00,

Equities tumbled in Europe SXXP,

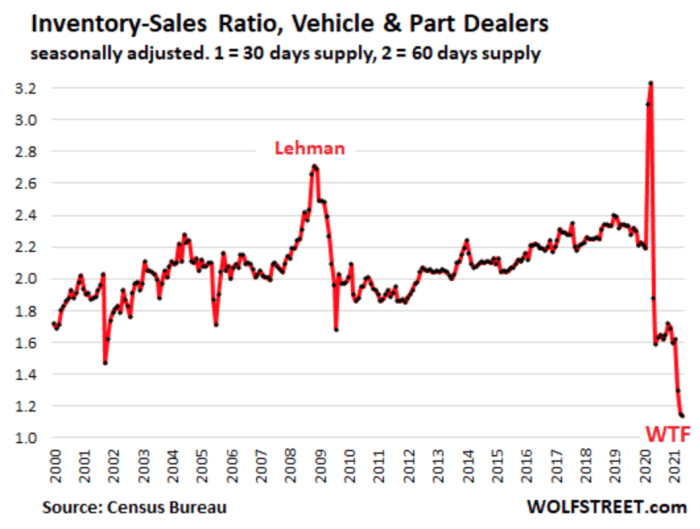

The chart

Retail sales spikes caused by the pandemic have led to shortages of all kinds. Our chart of the day, via Wolf Richter of the Wolf Street financial blog, shows the “catastrophic” condition of inventories at auto dealers — which before the pandemic made up more than one-third of all retail inventories.

Random reads

Tour de Franks: The world’s biggest bicycle race was almost disrupted by a sausage truck stuck on the winding roads of the Col De Romme.

Broke-chain technology: Malaysian police used a giant steamroller to destroy more than 1,000 crypto asset mining rigs seized from a property set up to steal electricity.

Need to Know starts early and is updated until the opening bell, but sign up here to get it delivered once to your email box. The emailed version will be sent out at about 7:30 a.m. Eastern.

Want more for the day ahead? Sign up for The Barron’s Daily, a morning briefing for investors, including exclusive commentary from Barron’s and MarketWatch writers.