According to the report, the industry is in the age of disruption with technology, changing consumption patterns and environmental, social and governance (ESG) considerations shaping the future of market players and inevitably determining success or the contrary.

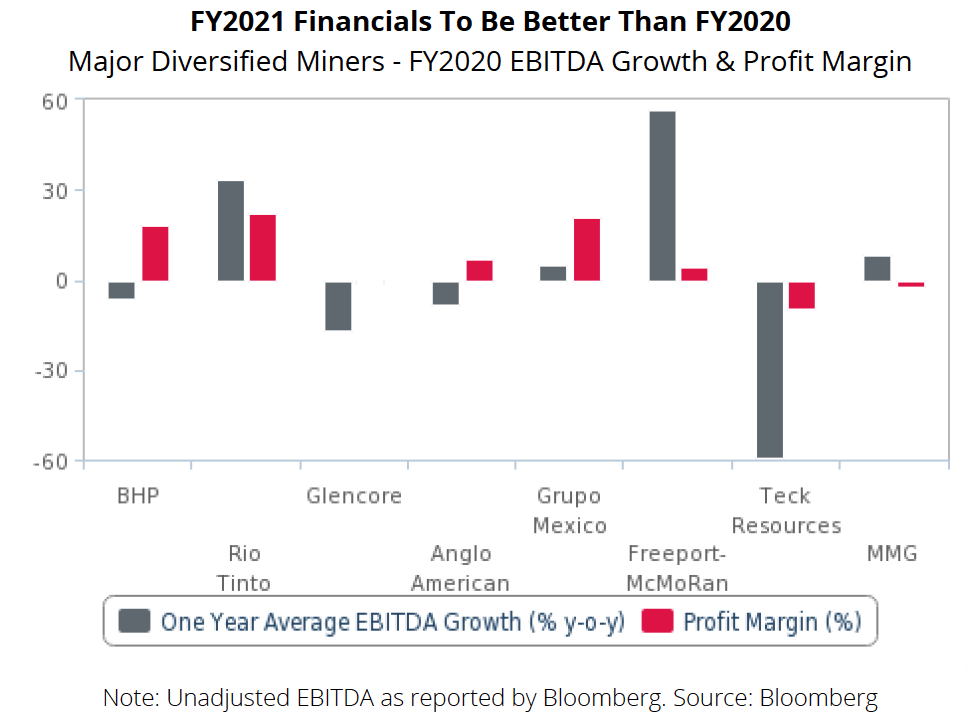

Major mining companies could weather the covid-19 pandemic better, primarily thanks to higher metal prices following the first quarter of 2020. For example, Rio Tinto’s (NYSE: RIO; LSE: RIO; ASX: RIO) net profit grew by 22% year on year in 2020 compared with a 41% year on year decline in 2019, while Anglo American (LSE: AAL), Freeport-McMoRan (NYSE: FCX), Norilsk Nickel (US-OTC: NILSY) and Vale (NYSE: VALE) registered net profits.

Fitch expects these financial results to be even stronger in FY2021-FY2022.

On the back of the performance, the miners had in recent months announced higher guidance for output and capital expenditures in 2021 and 2022 compared with 2020. As of April, Fitch’s bi-annual mining capex outlook was for capex by the top 30 miners to grow by about 23.7% year-on-year in 2021, after it broadly stagnated in 2020.

The updated guidance reflects more robust financials, low base effects, and a general vision to return to pre-planned levels of activity with the assumption that there would be no more lockdowns that could once again hamper miners’ capabilities, Fitch says.

Miners will increase investments in copper, lithium and nickel projects owing to the rising demand.

However, in taking a closer look at individual company capex figures, Fitch Solutions says the overall trend remains that companies are investing more in developing their existing assets than in exploring new ones.

Going forward, Fitch expects miners to increase investments in copper, lithium and nickel projects owing to the rising demand for these metals from the renewable energy, battery and electric vehicle sectors.

Trends to watch

Miners and metals companies are also likely to try and extract value out of the sustainability trends, Fitch says, as there will be pressure on mining companies to decarbonise, reduce their environmental impact and improve transparency.

That pressure will increase dramatically in the coming years, as downstream players aim to reduce Scope 3 greenhouse gas (GHG) emissions.

According to McKinsey & Co, mining is responsible for 4% to 7% of global GHG emissions regarding the sector’s Scope 1 and Scope 2 emissions. In comparison, including Scope 3 emissions links the industry to about 28% of total global emissions, according to Fitch.

Therefore, the agency expects first movers in this respect to enjoy a premium for their products in the future as downstream players demand low-carbon metals.

Mining capex will continue to target advanced technology that enables further efficiency gains, as industry leaders prioritise technology to remain competitive and better withstand price volatility.

First movers could enjoy a premium for their products in the future as downstream players demand low-carbon metals.

Fitch expects the acceleration of technological integration in the mining industry will widen the gap between the top low-cost producers and junior miners and improve the competitiveness of developed markets compared with underdeveloped markets.

Fitch Solutions suggests that Rio Tinto will remain the leader as the company boasts innovation and cutting-edge technologies in operations that can be matched by no other.

Going forward, however, cyber-risks, owing in part to the proliferation of new digital technologies, the increasing degree of connectivity and a material increase in the monetisation of cyber-crime, will become a more prominent cause for mining companies’ concern.

Meanwhile, rising resource nationalism will also be a significant risk to mining companies in the coming years. The regulatory space is ever-changing, with more governments looking to demand greater returns from the natural resources sectors in their jurisdictions.

In 2021, Fitch Solutions forecasts that this will accelerate as it expects an uptick in government intervention and resource nationalism amid the race to access critical and strategic minerals for the green and digital economy and as domestic political risk rises in the post-covid-19 world.