Such inaction in itself carries risks: failing to invest now will endanger the future supply of a number of commodities critical to achieving the ambitious net-zero goals set by government and investors alike, Kettle points out, and asks why is the industry so wracked by apparent doubt – and can a better balance between risk and reward be found?

Past sins and open promises driving industry behaviour

An aversion to risk in general – and to repeating the sins of the past in terms of capital destruction in particular – appears to be holding back the mining industry, WoodMac asserts. This is compounded by investors who, having been promised consistent dividend distribution through the cycle, are now hooked.

Expansion capex is in very short supply, Kettle says with miners starving themselves of the capital they need to develop future supply.

Kettle asserts the gap between current capex commitments and what’s needed to deliver a two-degree pathway (where the rise in global temperatures since pre-industrial times is limited to 2 °C) amounts to almost $2 trillion over the next 15 years.

Is risk passé, or here to stay?

The assessment of risk is both relative and absolute and comes with a large dose of perception, Kettle writes.

“Given the challenge of project development, particularly around the issue of ESG risk, there is a narrative in some circles that risk is somehow passé, that what counts most is whether you can actually mine in a given jurisdiction.”

“I’ve reflected on this a great deal. I don’t think risk itself is passé – in fact it’s very much front of mind for investors, most of whom recognise the interplay between risk and reward but err on the side of caution. I do agree that the ability to actually mine is hugely important. However, I would argue that risk comes first: the fact you are comfortable proceeding with a project, particularly in a higher risk jurisdiction, means you have already overcome risk hurdles and are comfortable with the risk-reward matrix presented. Only in that sense is risk passé.”

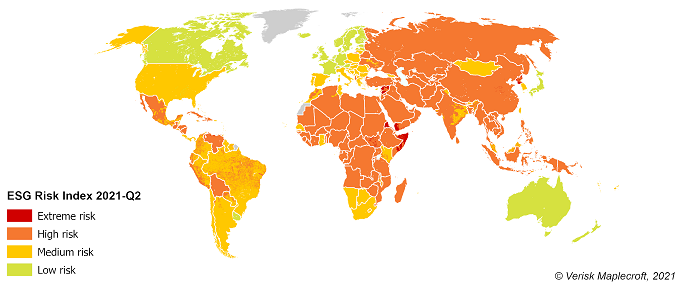

ESG risks: a minefield for mining industry stakeholders

Wood Mackenzie’s sister company Verisk Maplecroft undertakes a quantitative assessment of risk that takes into consideration all three ESG components (environmental, social and governance). The results are represented as a heat map, which demonstrates there are few places on the planet where mining companies can develop and operate mines with low ESG risk.

Risk: an intersect between subjectivity, objectivity and perspective

Appetite for risk varies, Kettle points out, as do opinions about the degree of risk inherent in any given project. For example, a small band of players have license to and appetite for operating in the Democratic Republic of Congo (DRC) – as well as domestic firms, Chinese, Russian and one or two Western players operate mines in the country.

Operating in the DRC and adhering to higher ESG standards than would otherwise be put in place could arguably have a de-risking effect. However, ultimately the DRC is viewed as a high-risk jurisdiction that most governments, investors, lenders and miners avoid – despite its extensive high-grade copper and cobalt resources.

While the players operating there would, Kettle maintains, argue that the DRC attaches manageable risk, the problem is that it does not matter whether they are comfortable with the DRC risk profile, what really matters is the fact that the broadly held view is that it is high risk.

Stakeholders must work together to de-risk supply

Kettle argues that, given the need to meet tough decarbonisation and ESG targets, Western governments, lenders, investors and consumers will need to get comfortable operating in jurisdictions where ESG issues are more complex.

Government support to de-risk investments in certain countries is a necessary catalyst to enable mining in as ESG-compliant a way as possible, Kettle says. Intergovernmental agreements, low-cost loans, export credit arrangements and other measures will enable stakeholders to obtain the guarantees they need to mitigate risk.

What naturally follows is that consumers and society become more comfortable that mining in these jurisdictions is being done ‘the right way’, Kettle says, and then, and only then, will the West be able to secure sufficient volumes of the raw materials needed to pursue the energy transition in the timescales envisaged.

“Essentially, the West could take a leaf out of China’s book in securing the necessary supply chain, albeit ensuring far higher ESG standards are applied.”

“This would involve governments curbing their natural reticence about stepping directly into business, and perhaps looking at risk through a different lens. “Fortes fortuna adiuvat”, as the Roman proverb says – fortune favours the brave – and bravery always comes with some risk. But with China already setting the pace in the energy transition race for raw materials, doing nothing is not an option for the West.”