Benzinga

Strong Earnings From Home Depot And Lowe’s, With Nvidia Waiting In The Wings

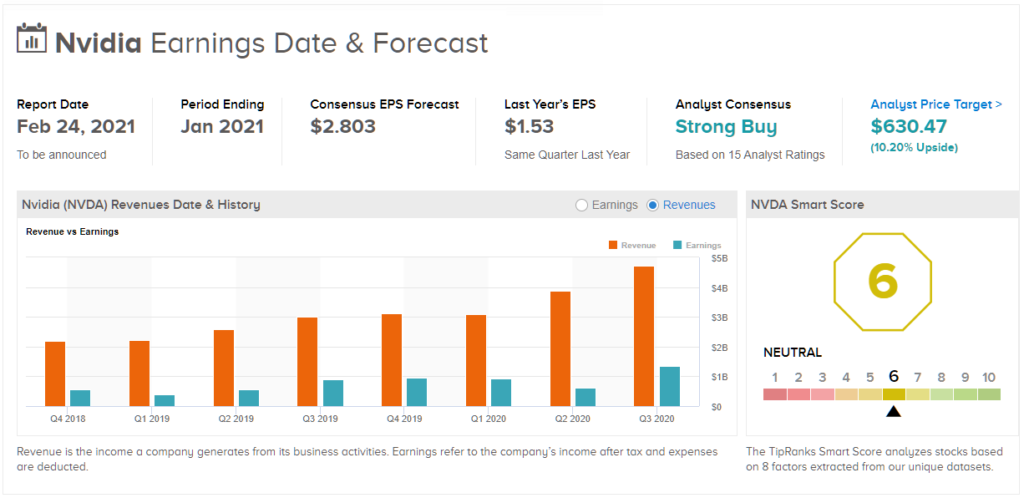

How do you follow up an amazing comeback like Tuesday’s? It’s hard, investors learned this morning. Overnight, stocks moved higher, then gave up their gains in the hour before the open as the 10-year Treasury yield spiked to 1.42%. This shows how sometimes momentum spills over into the morning after a sharp recovery, but doesn’t always last. There’s some solid earnings news in the mix, but otherwise not a lot of catalysts around to provide another boost. Volatility eased late yesterday, but this morning finds itself back on the rise. And 10-year Treasury yields look to be continuing their march forward, rising to 1.42% in the early going, This seems to be spooking stocks. It was almost exactly a year ago when we were last at these levels, right before the bottom fell out. Keep an eye on Tesla Inc (NASDAQ: TSLA) and Apple Inc (NASDAQ: AAPL) shares today. They’ve been bellwethers for the broader market lately, and their moves could have pretty wide influence. In a bit of late-breaking news, the U.S. Food and Drug Administration (FDA) said this morning that Johnson & Johnson’s (NYSE: JNJ) Covid vaccine has a “favorable safety profile,” The Wall Street Journal reported. FDA authorization could come as soon as this weekend, the newspaper said. We’ll see if that injects any strength into the market. Home Improvement Retailers Had Strong Q4 More earnings news, this time from Lowe’s Companies Inc (NYSE: LOW). Shares rose in pre-market trading after the home improvement company surpassed analysts’ estimates and stuck to its prior guidance. Same-store sales rose more than 28% in Q4. Meanwhile, Home Depot Inc (NYSE: HD) investors became the latest to fall victim to a stock losing ground even after a company reports solid earnings. This is a trend noted last week by research firm FactSet, with companies reporting positive earnings surprises generally getting punished over the last couple of months. In a lot of cases, you can chalk it up to stock prices building in strong expectations, but it’s tough to argue that with HD. Its shares have chopped around without much direction most of the last six months. HD’s results were impressive—comparable sales rose 24.5% year-over-year and overall sales rose nearly 20%. However, once again HD declined to give guidance, and that might have disappointed some investors. After the close, be on the lookout for earnings from chip maker NVIDIA Corporation (NASDAQ: NVDA). The company might be asked to provide an update on the industry-wide chip shortage, and discuss what analysts say has been strong gaming demand thanks to the stay-at-home economy. Shares have doubled over the last year, but recently fell from all-time highs. Before that, there’s more congressional testimony on tap from Fed Chairman Jerome Powell. He sounded pretty dovish yesterday, reinforcing what he’s been saying for weeks about the soft economic picture and low inflation. Turnaround Tuesday Afternoon When sports fans talk about comebacks, they might mention the 1986 Mets or the 1978 Yankees. Well, the stock market staged a phenomenal comeback of its own Tuesday after cratering early on, and that sets the stage for what could be an interesting Wednesday. Yesterday’s rebound, by the way, kept the S&P 500 Index (SPX) from suffering a six-session losing streak just a few weeks after it posted a six-session win streak. It’s really unbelievable how the Tech and reopening stocks rallied back so significantly in the last three hours of the session Tuesday. Some analysts claimed it had to do with Powell “easing inflation concerns” in his testimony to Congress. That doesn’t quite match what happened, though, because stocks were selling off when he spoke and then rallied when he stopped talking. That’s not to say Powell caused the early selloff, but he might not deserve credit for the comeback, either. Instead, it might have reflected that there’s so much money sloshing around—with the expectation of more arriving soon with the fiscal stimulus—and people are trying to put that money to work. Higher fixed income yields might have some people thinking of investing in those products, but at the end of the day the dominant market sentiment seems to be that equities remain the best game in town. As we start approaching the end of Q1, people may be looking around wondering what else they should do with this cash, and that’s why more money might have come in yesterday afternoon following the morning dip. Getting back to Powell, many investors likely took comfort in his words about keeping policy accommodative, but inflation fears were very possibly a factor helping drive stocks downward earlier this week and shouldn’t be discounted. Tuesday’s late snap to the upside doesn’t mean we’re out of the woods. Today could be critical as far as momentum for the rest of the week. Momentum Change: Can It Continue? Often when the week begins with a couple of soft days and then momentum shifts higher, you see a strong open on Wednesday before stocks sell off again later in the session. It’s possible any continued move higher today could end up getting slapped back down, if that pattern holds. It seems like there’s still a lot of money on the sidelines waiting for a bigger selloff, and it would be dangerous to discount chances for one as the market heads into March. These last few days served as a wakeup call to investors about how quickly things can move down, especially seeing the momentum change for TSLA and how that hurt the SPX (see more below). Some people will say, sure, the market fell but continues to bounce on moves lower, and that’s hard to rebut. Buying the dip has worked. It’s hard to bet against that happening again, but you can’t rely on history to always repeat. Like any strategy, buying the dip works…except when it doesn’t. The technical action yesterday was also pretty interesting, with the Nasdaq (COMP) and S&P 500 Index (SPX) both briefly dropping below their 50-day moving averages and then coming back to close above those trendlines. The 50-day MA for the SPX is near 3796 and for the COMP is near 13,003, so both of those regions might be worth monitoring if the market gets slammed again. For now, it’s technically positive to see the COMP and SPX manage to claw back from below those levels intraday Tuesday. It’s also interesting to see how volatility performed, with the Cboe Volatility Index (VIX) starting off yesterday much higher (above 26 at one point), and then turning back down to near the 23 level. That’s still above its recent lows just below 20, and the futures complex going out the next few months still builds in a lot of uncertainty. Some outer months trade above 29 (see chart below). Stay-At-Home Stalwarts Bounce Back – For Now Getting back to individual stocks for a bit, keep in mind that two of the stocks rebounding yesterday were ones we’ve heard a lot about as “stay at home” ones over the last year: Peloton Interactive Inc (NASDAQ: PTON) and Zoom Video Communications Inc (NASDAQ: ZM). These two rallied back yesterday but have been under some pressure lately as the market psychology seems to be favoring stocks like casinos and airlines that could benefit from reopening. Because PTON and ZM rallied so significantly Tuesday from their early-session lows, it would be good to see them at least tread water the rest of the week. If they move lower after that big recovery, it would probably be a bad sign for them. Profit-taking might have hurt PTON and ZM early this year, and it’s almost certainly hit the broader Tech sector. The rally in Treasury yields played a role, and the slight step back in the 10-year yield to 1.34% by late Tuesday from highs above 1.38% earlier in the week might have let some of the pressure out of the yield balloon weighing on growth stocks. Powell’s dovish words about weak employment growth and “soft” inflation certainly could have been behind Tuesday’s yield decline and subsequent Tech rebound, but remember, Powell and company don’t completely control borrowing costs. Many investors anticipate bigger supplies of debt as more stimulus comes on line, meaning maybe more room for yields to rise than fall. CHART OF THE DAY: MORE VOLATILITY AHEAD? Aside from its brief encounter with the mid-30s during the recent short-squeeze scare, the Cboe Volatility Index (VIX) has been hanging out in the low-to-mid 20s recently—still above its long-term average around 20, but well off levels seen in 2020. But here’s something: A month ago the VIX futures (/VX) curve flattened out at 27. As of yesterday’s close, however, traders are pricing those deferred-month contracts around 29.5. It could be that the recent runup in Treasury yields has added a new haze to the economic outlook. Data source: Cboe Global Markets. Chart source: The thinkorswim® platform. For illustrative purposes only. Past performance does not guarantee future results. Penny for Your Thoughts: If you followed the short-squeeze surge last month, you may be aware of a new craze going on in micro-caps and so-called “penny” stocks. Way-off-exchange venues, where lightly regulated companies have repeatedly been drawn into social media-fueled trading vortexes, saw more than 1 trillion shares change hands in December for the first time in a decade, Bloomberg reported. It happened again in January. This month, daily volume is tracking 64% above those levels, a pace that could push the monthly total toward 2 trillion. The Securities and Exchange Commission (SEC) recently suspended trading in one firm, saying “social media accounts may be engaged in a coordinated attempt to artificially influence” its share price. Regulatory halts in shares that are traded over-the-counter—which is the case for a lot of these penny stocks—aren’t entirely unusual or unheard of. The SEC is now looking at that because they’re questioning what’s driving some of the behavior. As a long-term investor, it’s good practice not to get caught up in these types of crazes, or in trading off-exchange products. It can truly be the Wild West out there. Tech Not Alone: Utilities are taking a big hit along with Tech lately, and surprisingly for pretty much the same reason. as rising bond yields are starting to reach territory where they could potentially compete with dividends for yield seekers. The current S&P 500 dividend yield of 1.5% isn’t far above the 10-year Treasury yield of 1.36%, and some investors prefer getting their yield from fixed income, which tends to have a lower risk profile than stocks (though remember no investment is risk-free). Utilities have a reputation of being a “bond proxy,” meaning they sometimes trade more like bonds than stocks, and yields are the primary reason some people invest in this sector. That means they’re more vulnerable to interest rates than most other sectors of the S&P 500. Utilities are down 5% in the last three months, by far the worst performance of any sector over that time. Consumer Staples, another interest rate-sensitive category, are the only other sector in the red during that time period. Tesla Throws its Weight Around: When Tesla Inc (NASDAQ: TSLA) joined the S&P 500 Index (SPX) last December, it was the highest initial weighting ever for a new entrant (1.6%). It’s also among the highest in terms of price-to-earnings (P/E) ratio (1,100), and it’s been among the most volatile stocks in the SPX. Oh—and it’s the 6th most valuable public company in the U.S. by market cap. That’s part of the dichotomy of TSLA—its fundamental metrics and growth narrative are reminiscent of a start-up, but its sheer size puts it in the company of cash cows such as Apple Inc (NASDAQ: AAPL) and Microsoft Corporation (NASDAQ: MSFT). When TSLA was added to the SPX, we suggested it could impact the volatility of the broad-based index. Case in point: At its depths yesterday morning, TSLA was down 20% over two sessions. With its current weighting of 1.65, a back-of-the-napkin calculation suggests TSLA shaved as much as 13 points off the SPX before the midday rally. While that may sound small in the context of yesterday’s 90-point range in the index, when you consider the SPX is made up of roughly 500 stocks, it’s still quite an impact for one company’s shares. In contrast, it’s not uncommon for a big move in a single name to have an outsize impact on the 30-stock Dow Jones Industrial Average ($DJI). TD Ameritrade® commentary for educational purposes only. Member SIPC. Photo by Annie Gray on Unsplash See more from BenzingaClick here for options trades from BenzingaMarch Outlook: Economic Optimism Surrounds New Stimulus, But Yield Surge Hits Tech’Tech Check’ Continues, With Apple, Tesla Under Pressure Ahead Of Powell Testimony© 2021 Benzinga.com. Benzinga does not provide investment advice. All rights reserved.